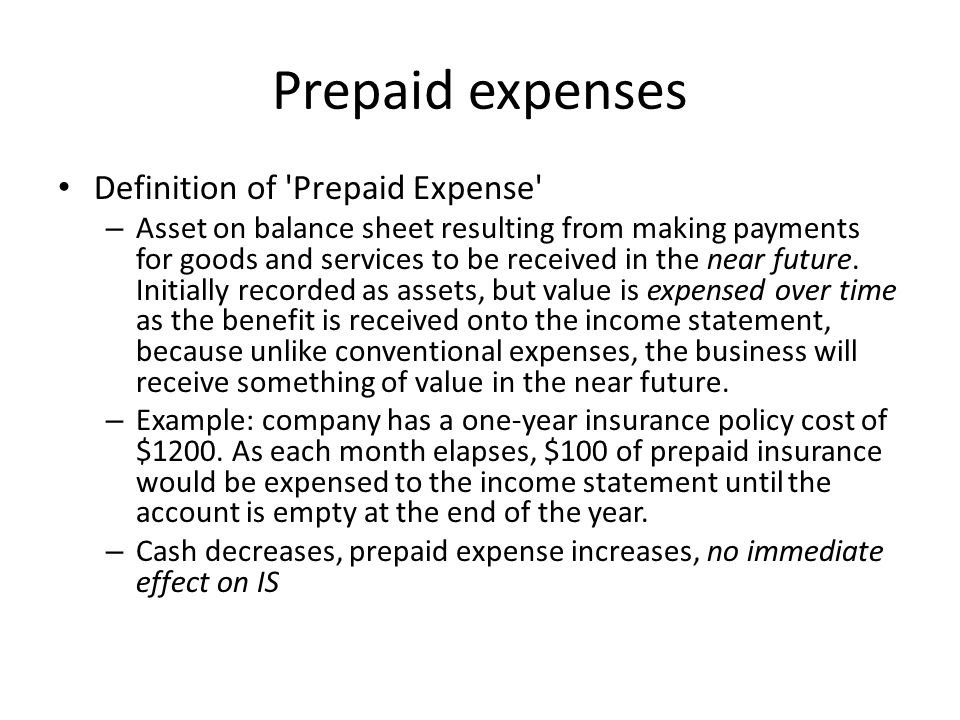

Content

It is done irrespective of whether actual cash is paid or not. Total liabilities are the combined debts, both short- and long-term, that an individual or company owes.

All “mini-ledgers” in this section show standard increasing attributes for the five elements of accounting. The double-entry system can reduce accounting errors because the balancing-out step works like a built-in error check. Our seasoned bankers tap their specialized industry knowledge to craft customized solutions that meet the financial needs of your business.

Accrued liabilities are only reported under accrual accounting to represent the performance of a company regardless of their cash position. They appear on the balance sheet under current liabilities.

These payments don’t generate operating income, so they are recorded as a non-operating expense. Operating expenses include all costs that are incurred to generate operating revenues like merchandise sales. Expenses accounts are equity accounts with adebitbalance. Expense accounts are consideredcontra equity accountsbecause their balance decreases the overall equity balance. In other words, debiting an expense account increases the balance instead of decreasing it like most other equity accounts. Accountants like numbers and need to track everything back to a transaction.

Accountants close out accounts at the end of each accounting period. This method is used in the United Kingdom, where it is simply known as the Traditional approach. Advertising consists of payments made to another company to promote products or services. Just about every company advertises their products or services in one way or another. These payments are recorded as operating expenses because they help sell generate operating revenues.

HOME FEDERAL BANCORP, INC. OF LOUISIANA MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS (form 10-Q).

Posted: Fri, 10 Feb 2023 19:55:04 GMT [source]

If a contingent liability is only possible, or if the amount cannot be estimated, then it is only noted in the disclosures that accompany the financial statements. Examples of contingent liabilities are the outcome of a lawsuit, a government investigation, or the threat of expropriation. A warranty can also be considered a contingent liability. The offsetting debit is to the interest expense account, and indicates the amount of interest expense accrued by a business, but not yet billed to it by a lender. AT&T clearly defines its bank debt that is maturing in less than one year under current liabilities. For a company this size, this is often used as operating capital for day-to-day operations rather than funding larger items, which would be better suited using long-term debt. However, money given to an employee via an expense account is not a liability for a future date.

An asset is anything that your company owns that can be converted to cash or has the capacity to generate revenue. They include tangible and intangible things of value gained through the company’s ongoing transactions. Different types of businesses will have different accounts. Many industry associations publish recommended charts of accounts for their respective industries in order to establish a consistent standard of comparison among firms in their industry.

It is categorized as current liabilities on the balance sheet and must be satisfied within an accounting period. A common example of this phenomenon is in the accounting for sponsorship agreements. Even though a company may be contractually obligated to sponsor an event for five years, the company will not record a liability up-front In Accounting, What Is the Difference Between a Liability Account and an Expense Account? for the agreement. The company will only record the liability for the benefit received but not paid. There are five types of accounts that show up on both your balance sheet and income statement. They consist of assets, liabilities, equity, revenue and expenses. Is the cash account an asset, a liability, or an owner’s equity account?

An asset account reflects the value of resources owned by a company and is expected to provide future economic benefit. Examples include cash, accounts receivable, inventory and property. Accounts payable are considered liabilities and not expenses. Because accounts payables are expenses you have incurred but not yet paid for. Expenses are periodic and are listed on the balance sheet as Accrued Expenses as a current liability in the balance sheet. Whereas accounts payable are a part of the everyday process as a current liability on the balance sheet. Examples of liabilities are accounts payable, accrued liabilities, accrued wages, deferred revenue, interest payable, and sales taxes payable.

The term “T-account” is accounting jargon for a “ledger account” and is often used when discussing bookkeeping. The reason that a ledger account is often referred to as a T-account is due to the way the account is physically drawn on paper (representing a “T”). The left column is for debit entries, while the right column is for credit entries. The below example illustrates a financial transaction in which a catering company provided its services for a client’s party.

The information recorded in these daybooks is then transferred to the general ledgers, where it is said to be posted. Not every single transaction needs to be entered into a T-account; usually only the sum for the day of each book transaction is entered in the general ledger. In the below example of a journal entry, a business owner paid their employee’s salary. Cash was used to pay the salary, https://business-accounting.net/ so the asset decreases on the credit side , and salary expenses increase on the debit side . Accrued liabilities are other balance sheet liabilities that must be paid but don’t have a direct invoice. For example, on my company’s balance sheet I have accrued liabilities for items such as employee tax withholding that is withheld from paychecks weekly but only paid to the government quarterly.

In simplistic terms, this means that Assets are accounts viewed as having a future value to the company (i.e. cash, accounts receivable, equipment, computers). Liabilities, conversely, would include items that are obligations of the company (i.e. loans, accounts payable, mortgages, debts). To determine whether to debit or credit a specific account, we use either the accounting equation approach , or the classical approach . Whether a debit increases or decreases an account’s net balance depends on what kind of account it is. The basic principle is that the account receiving benefit is debited, while the account giving benefit is credited.